All posts

2025-12-10

4 min read

SMEs count the cost of Brits’ ‘Fear of Messing Up’ (FOMU) at checkout

Our latest research reveals that many UK consumers feel anxious about making mistakes when paying by manual bank transfer. This lack of confidence is driving abandoned transactions and undermining trust in the small businesses they buy from – while simple human errors continue to cause failed payments.

Read more

2025-12-03

2 min read

Fidelity introduces Tink’s Pay by Bank for account top-ups

Tink and Fidelity International have partnered to enable account top-ups via Pay by Bank for Fidelity’s Personal Investing customers and advised clients on the Fidelity Adviser Solutions platform.

Read more

2025-11-20

3 min read

Tink powers the UK’s first cVRP transaction with Visa A2A

In partnership with Visa, Kroo Bank, and Utilita, we’ve just helped demonstrate the UK’s first commercial variable recurring payment (cVRP) using the Visa A2A solution – and it’s a big step forward for how people make regular payments.

Read more

2025-10-30

2 min read

Coinbase and Tink partner to launch Pay by Bank crypto payments in Germany

Coinbase and Tink have partnered to launch Pay by Bank in Germany, enabling secure, fast crypto purchases directly from users’ bank accounts and expanding access to the cryptoeconomy with a seamless, mobile-first experience.

Read more

2025-10-20

2 min read

Splitwise expands Pay by Bank across France, Germany, and Austria with Tink

Splitwise is expanding its partnership with Tink to bring seamless Pay by Bank payments to users in France, Germany, and Austria, following a year of rapid growth of our partnership in the UK. This move enables millions more people to settle shared expenses instantly and securely within the Splitwise app, thanks to our open banking technology.

Read more

2025-10-07

7 min read

Beyond instant: Building reliable Pay by Bank payments

As instant payments roll out across Europe, merchants still face challenges with reliability and settlement. Our Smart Routing and Risk Signals products provide a reliability layer for Pay by Bank, optimising payment routes and blocking likely-to-fail transactions.

Read more

2025-09-18

2 min read

Vipps MobilePay selects Tink to power Pay by Bank for P2P in Finland

We are delighted to announce a new partnership under which Vipps MobilePay will use Tink’s Pay by Bank to power peer‑to‑peer (P2P) payments in Finland.

Read more

2025-09-03

6 min read

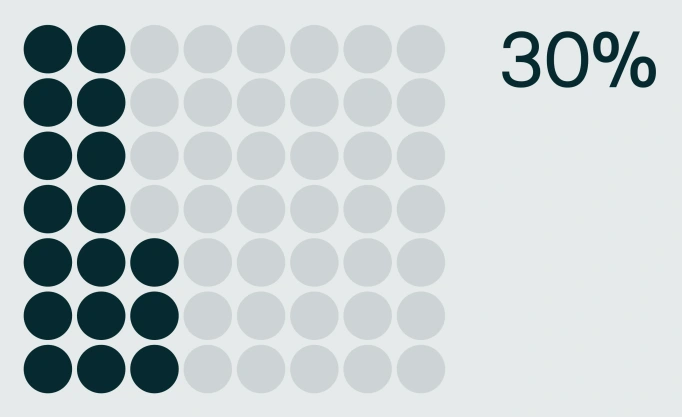

Brits’ ‘fear of fraud’ cost UK SMEs £6.15bn in the last financial year

The latest research and economic analysis from Tink shows that UK SMEs relying on outdated manual bank transfers as a primary method of payment lost out on an estimated £6.15 billion in sales last year.

Read more

2025-07-01

2 min read

Tink and Chip partner to power seamless account top-ups with open banking

Chip, the award-winning wealth app, is now using Tink’s open banking technology to offer users a faster, more secure way to top up their accounts.

Read more

2025-06-18

2 min read

Video – How Snoop is unlocking smarter saving with variable recurring payments

With the launch of variable recurring payments (VRP), Snoop is introducing a smarter, more flexible way for people to build their savings – and making the most of Tink's open banking solutions in the process.

Read more

2025-06-09

11 min read

The case for “Pay by Bank” as a global term

Thomas Gmelch argues that "Pay by Bank" should be adopted as a standard term for open banking-powered account-to-account payments to reduce confusion, build trust, and boost adoption across the industry.

Read more

2025-06-02

3 min read

Tink joins Visa A2A – what it means for Pay by Bank and VRP

Visa A2A brings an enhanced framework to Pay by Bank and variable recurring payments (VRP) in the UK, and Tink is excited to be one of the first members of this new solution.

Read more

2025-05-28

2 min read

Tink and Adyen partner to bring Pay by Bank to Vodafone customers in Germany

Tink and Adyen have announced a partnership with Vodafone, a leading telecoms company, to offer their customers in Germany the option to pay their prepaid tariff and outstanding postpaid balances using Pay by Bank.

Read more

2025-03-20

4 min read

Tink hits 10,000 merchant milestone for open banking payments

As the adoption of open banking payments surges, we've hit a new milestone as 10,000 merchants choose Pay by Bank – plus a new €100M daily peak for our payment initiation services

Read more

2025-02-12

1 min read

Video: Francois Tornier on his time at Tink & Visa, and the future of A2A payments

Meet Francois Tornier, our VP Open Banking, in this video to find out more about his journey with Tink and Visa, expanding account-to-account payments, and the challenges of navigating a complex ecosystem.

Read more

2025-02-06

6 min read

Introducing User Match: Built-in name verification to make security fast and easy

Discover how the latest feature of our verification products, User Match, is improving security by verifying users' names when adding bank accounts, reducing fraud and enhancing account protection.

Read more

2025-02-05

6 min read

Merchants invest in payment upgrades as younger generations prioritise sustainability and security for luxury purchases

The latest findings from our peak season survey suggest that younger generations are reshaping the luxury market by prioritising quality, sustainability, and secure payment experiences. With cost-of-living pressures, these discerning shoppers demand more than just premium products, pushing high-end merchants to upgrade their payment systems to stay competitive.

Read more

2025-01-15

1 min read

Guide – How to optimise verification with open banking

Download our new account verification guide to learn how to streamline your operations, reduce risk, and enhance customer experience with the help of open banking-powered solutions.

Read more

2024-12-17

7 min read

User experience: Wealthify empowers customers’ financial wellness with Pay by Bank

Tink partner Wealthify uses Pay by Bank for the optimal PFM, investment and saving experience, thanks to easy account top ups and secure account-to-account payments.

Read more

2024-12-11

6 min read

Three in four high-end merchants optimistic about peak season

New research from Tink shows that, this festive season, quality is trumping quantity as many cost and climate-conscious consumers choose to invest in higher-quality goods, even if that means purchasing fewer items overall.

Read more

2024-11-19

12 min read

From authentication to authorisation: Navigating the changes with eIDAS 2.0

Discover how the eIDAS 2.0 regulation is set to transform digital identity and payment processes across the EU, promising seamless authentication, enhanced security, and a future where forgotten passwords and cumbersome paperwork are a thing of the past.

Read more

2024-10-14

4 min read

How Northmill’s loan book performance is reaching new heights with Tink

As consumers choose lenders and financial services for hyper-personalised, intuitive and convenient UX, Northmill partners with Tink for an optimal customer experience – and boosts its loan book performance to boot.

Read more

2024-10-08

6 min read

Lending essentials: how enriched data solutions help lenders tackle constraints

Enhancing your affordability assessment with Tink’s data-enriched solutions helps you put an end to inaccurate data, prevent fraud in loan origination and stay compliant – read on to explore the benefits.

Read more

2024-10-01

4 min read

Meet Merchant Information: providing bank customers with elevated transaction visibility

Tink has today launched Merchant Information, a solution of our Consumer Engagement offering which provides consumers with more detailed information about their transactions.

Read more

2024-09-24

4 min read

Why Pay by Bank fits luxury retail like a glove

Pay by Bank offers a solution that addresses the potentially higher transaction fees and fraud risks while enhancing the customer experience for luxury retailers.

Read more

2024-09-18

14 min read

Connecting the dots: how UX optimisations are driving success rates

We’ve previously explored small tweaks that get big results in open banking conversion rates. This deep dive drills further into how to reduce friction – and improve success rates through a fresh round of incremental changes in our UX.

Read more

2024-09-04

2 min read

CTS EVENTIM adds Tink’s user-friendly Pay by Bank service to its checkout options – giving fans even more choice

Collaborating with Tink, a market-leading payment services and data enrichment platform, CTS EVENTIM has now added Pay by Bank to its checkout process.

Read more

2024-09-03

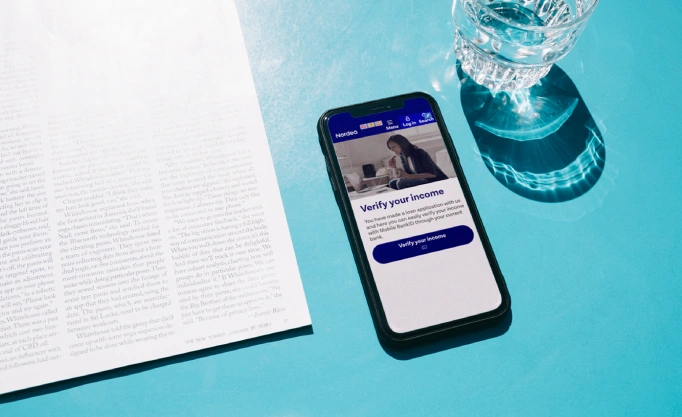

5 min read

Customer interview – Nordea on consumer engagement

We spoke to Nordea Product Manager Sami Mikkonen about enhancing their mobile app using open banking technology, focusing on improving consumer engagement and financial management.

Read more

2024-08-20

7 min read

UK bank customers could be almost £24.5 billion better off per year – through the power of digital financial management tools

Tink’s new research is telling for banks, revealing that consumers now demand more digital financial management tools to support their personal finance goals.

Read more

2024-08-12

11 min read

Six ways open banking helps remittance

Learn all about remittance, and how open banking can help it happen more smoothly with six of our best tips. From reducing friction, to simplifying compliance processes, and much more.

Read more

2024-08-05

5 min read

Feature update: Savings Goals elevates your money management experience

Reaching financial goals can be daunting – so we’ve updated Savings Goals, a feature of Tink Money Manager designed to help banks empower customers to proactively save and achieve financial wellness.

Read more

2024-07-29

6 min read

Not just another payment method – six reasons why leading PSPs are prioritising Pay by Bank

In the second article of this series, we focus on why leading Payment Service Providers (PSPs) – like Adyen and Stripe – are introducing Pay by Bank to their checkout options (and why this is important for their merchants too).

Read more

2024-07-29

6 min read

Pay by Bank in 2024 - the current status and outlook

Sometimes called open banking payments, or account-to-account (A2A) payments, Pay by Bank is now the more common industry term in ecommerce. Tink is one of the leading providers, and here we provide an overview of one of the fast-growing payments technologies in the first of a new blog series.

Read more

2024-07-24

3 min read

Tink supports DKB with optimising construction loan processes

Top 20 German bank, Deutsche Kreditbank AG (DKB), teams up with Tink to give construction loan seekers a digital, frictionless application process, based on real-time data.

Read more

2024-07-22

1 min read

Commercialising open finance – a VCA report

Tink worked with Visa Consulting and Analytics on a new white paper which details the state of play, direction of travel, and best open finance practices from around the world.

Read more

2024-07-17

2 min read

Banking on engagement

This Tink white paper introduces new consumer and retail banking executive research from key European markets, setting the scene for banks to take the next step with Personal Finance Management (PFM).

Read more

2024-06-20

6 min read

Engaging Gen Z: Tink’s new data on the biggest challenge for bankers in 2024

Tink’s new data identifies Gen Z as key for the banking industry, highlighting the importance of ensuring digitised, personalised features – read more and access the complete research here.

Read more

2024-06-19

7 min read

Borrowers and the cost of living: setting the scene for responsible lending in Sweden

Prioritise investing in data-driven lending models with Tink to make more informed credit decisions, enabling credit access to those who can afford it, while protecting struggling borrowers from getting into financial distress.

Read more

2024-05-30

5 min read

Meet Variable Spend: our latest feature for intelligent expense tracking

Expense tracking can be detailed as well as intuitive – say hello to Variable Spend, a new feature of Tink Data Enrichment designed to help banks offer their customers more insight.

Read more

2024-05-28

12 min read

Risk decisioning essentials: our latest categorisation model updates to help you get ahead

Confident decisions, top quality reports and going to market faster are just some of the benefits Tink’s new categorisation model has for lenders – deep dive into the world of generative AI, multilingual models, and more with this guide.

Read more

2024-05-09

5 min read

David van Damme – unlocking the potential of digital lending in Central Europe

Our new Banking & Lending director for the Netherlands and DACH region, David van Damme, shares his insights on these innovative markets, why they’re different and how digitalisation is changing the lending landscape.

Read more

2024-05-02

3 min read

TransferGo and Tink partner for international money transfers

TransferGo, the global fintech empowering a world on the move, has partnered with Tink to add Pay by Bank to its payments offering. Pay by Bank is now live for UK TransferGo customers, introducing a new way to more securely and quickly send money internationally.

Read more

2024-04-22

4 min read

Splitwise and Tink partner to make paying back friends and family easier than ever

Splitwise, a popular app for sharing bills and expenses, and Tink have partnered to bring Pay by Bank to Splitwise users. This enables millions of Splitwise users to initiate direct payments to friends and family from within the Splitwise app.

Read more

2024-04-16

4 min read

Jennifer Thunander – delivering the goods

How does Tink make sure that its technical integration is successful? That’s where delivery teams, overseen by people like Jennifer, come in. Here she tells us about her role and ensuring that Pay by Bank journeys are as smooth as possible.

Read more

2024-04-10

7 min read

Thomas Gmelch - how open banking can change the instant payment experience in Germany

We sat down with Thomas to chat about the challenges facing our customers in Germany, and how our newly launched Risk Signals product is coming to the rescue.

Read more

2024-04-08

6 min read

How the Instant Payments Regulation will change the EU payments landscape

We explore the details of the Instant Payments Regulation, as well as its benefits for consumers and PSPs – such as increased convenience, more innovation in the market, and reduced costs.

Read more

2024-03-20

1 min read

The ultimate guide for building the future of recurring payments

Variable Recurring Payments, powered by open banking, have huge potential for merchants and consumers in the UK. Read our VRP guide to find out how they work and why they are important.

Read more

2024-03-07

6 min read

Smart moves with smart meters: how commercial VRP could support pay-as-you-use billing models

Discover how variable recurring payments can transform smart meter billing into a more flexible user experience – and utility providers more ways to support financially vulnerable customers.

Read more

2024-03-06

3 min read

Deutsche Bahn and Tink partner for direct debit setups

Deutsche Bahn has teamed up with Tink for Account Check - enabling instant, easy and secure account onboarding. DB Connect, part of the Deutsche Bahn Group, runs some of Germany’s largest modern mobility sharing services including ‘Flinkster’, Germany’s largest car sharing network and ‘Call a Bike’, one of the biggest bike sharing systems in the country.

Read more

2024-03-05

5 min read

Serving younger borrowers: the impact of inaccessible lending

Streamline risk decisioning as a lender to lower operating costs using data-driven, digital loan origination, affordability assessment and income verification.

Read more

2024-02-27

4 min read

Meet Jack Spiers – Tink’s new UK&I Banking & Lending Director

We spoke to Jack about working with some of the largest financial institutions in the world, optimising our banking relationships together with Visa, and what excites him about the future in our industry.

Read more

2024-02-21

10 min read

The full SPAA treatment – Tink signs up for new EU scheme

Tink has become one of the first participants of the European Payments Council’s SPAA scheme. We explain why SPAA was needed and how it could be the catalyst to transform account-to-account payments in the European Union.

Read more

2024-02-20

5 min read

Billing and the cost of living: 2/3 of Brits want support from utility providers

Empower your customers through the cost of living with more options in energy billing and improved UX with variable recurring payments.

Read more

2024-02-12

10 min read

Building a more inclusive and diverse fintech industry

Hear from Tinkers who are closely involved with improving inclusion in the fintech industry and educating allies. While talking about their personal experiences, they also provide advice for members of the LGBTQIA+ community looking to enter the fintech arena.

Read more

2024-01-31

6 min read

Introducing Risk Signals: minimising fraud risk

Tink has launched Risk Signals, a rules-based engine that unlocks instant payment experiences while minimising risk – and already in use by Tink customers like Adyen.

Read more

2024-01-26

7 min read

How the EU digital identity wallet could change the way we pay

eIDAS 2.0 and the EU Digital Identity Wallet are coming and they have the potential to revolutionise the digital payments landscape, making transactions more secure than ever before. Find out what this means for payments, and for consumers and businesses alike.

Read more

2024-01-18

1 min read

How to create a winning Pay by Bank user experience

In this webinar our Tink team of Jaia Lloyd, Varun Atrey and Kevin Ward discuss how Pay by Bank (account to account payments) can vastly improve your user journey and demo how it works.

Read more

2024-01-16

4 min read

Level up your lending – and meet the challenges of fraud

Prevent fraud in loan applications with data enrichment tools from Tink – while enhancing your affordability assessment, building better UX and future proofing consumer loans for the digital age.

Read more

2024-01-02

8 min read

2024 – what’s on the horizon for payments and data-driven financial services?

From Pay by Bank and VRP, to risk assessments, sustainability and money management tools, 2024 looks set to be the year when data-driven financial services hit the mainstream.

Read more

2023-12-21

5 min read

Three key 2024 milestones in EU payments regulation

Looking ahead to next year’s financial regulation in the European Union, there are three important developments set to shape the future of payment initiation services – Instant Payment Regulation, EU Digital Identity Wallet, and the SPAA scheme.

Read more

2023-12-20

1 min read

Lending, levelled up

Tink's new lending white paper – with fresh research from the UK, France, and Germany – details how to elevate affordability assessments with enriched data, and why it’s more important than ever.

Read more

2023-12-04

5 min read

Livia Kathi – how to accelerate adoption of Pay by Bank

Livia Kathi, Tink’s Product Solutions Director, is spearheading our Pay by Bank drive in the challenging realm of ecommerce. Learn more about the crucial factors of user experience, building trust, and incentives.

Read more

2023-12-04

1 min read

Discussing sustainable banking with ecolytiq

In our latest webinar, we’re joined by David Lais, Co-Founder & Managing Director of ecolytiq to discuss how we have partnered to create a seamless way for banks to seize the opportunity and offer combined financial and sustainability coaching – and what we can expect for the future.

Read more

2023-11-21

2 min read

The ultimate Pay by Bank UX guide

At Tink, we’re excited about Pay by Bank. Our new, in-depth UX guide tells you how to make the most of this innovative payment solution.

Read more

2023-11-17

8 min read

Savings Banks Group takes the stage with Tink at Nordic Banking Forum 2023

Open banking tools like Tink Money Manager and Tink Data Enrichment help its partners, like Savings Banks Group, offer streamlined user experiences that coach consumers towards financial wellness.

Read more

2023-11-16

5 min read

Investments and the cost of living: why everyday investors are being forced to cash in

Investment platforms can avoid losing people to poor user experience – let open banking tools make your payments friction free, while your customers focus on their financial wellness.

Read more

2023-11-09

7 min read

Peak retail season: the cost of living and high volume returns

Prep for Black Friday and 2023 end-of-year sales with new data from Tink, and discover the benefits of Pay by Bank for seamless refunds and returns.

Read more

2023-11-02

4 min read

Sofia Sundström – Our obsession with quality in connectivity

Overseeing our ever-growing network of connections to banks is Sofia Sundström – we spoke to her to find out more about what sets Tink apart in this area, and why it’s so important to be a 'data nerd'.

Read more

2023-10-25

7 min read

A closer look at UK lending in the cost-of-living crisis

New research shows that one-in-four UK borrowers are using credit to cover essential spending, while 16% take out a loan to make ends meet. For lenders, there is increasing worry around fraud and a desire to improve risk decisioning models.

Read more

2023-10-23

8 min read

What you need to know on rescoping Account Information Services for a future open finance framework

Following the European Commission's PSD3, PSR, and FIDA proposals, here we examine some key considerations surrounding the potential transition of account information services (AIS) from PSD3 to FIDA.

Read more

2023-10-19

7 min read

Introducing Tink Loans – streamline consolidation with our new product

With Loans, lenders and brokers can gain access (with user permission) to applicants’ data within minutes, potentially leading to higher conversion, reduced friction, and a more holistic view of a user's running liabilities.

Read more

2023-10-11

6 min read

Smoother transfers are here with Tink Investments

With our new Investments product, neobrokers and wealth managers can use data-driven open banking to perform investment transfers and net worth consolidation in a quicker, more seamless manner that benefits the consumer too.

Read more

2023-10-03

7 min read

Direct debit cancellations: a guide to customer success with open banking

The cost-of-living crisis is impacting direct debits, but open banking tools can enable businesses to safeguard revenue while supporting customers. Read Tink’s guide to the solutions that can help.

Read more

2023-09-21

3 min read

Meet Christophe Joyau, Tink’s Senior Vice President of Banking & Lending

Christophe Joyau has played a crucial role in our transition from serving individual customers to business customers and building a B2B SaaS function – he told us about it and what it’s like working with Visa.

Read more

2023-09-14

6 min read

New streamlined authentication journey makes open banking payments even faster

Secure open banking payments are now even faster with streamlined authentication – optimise your payment journey and increase returning customers with Tink’s Pay by Bank-powered tools.

Read more

2023-09-12

3 min read

Scaling your services: how to offer your customers financial coaching

Help your customers manage the cost of living with open banking technology like Tink Data Enrichment, and offer them personalised financial coaching.

Read more

2023-09-05

12 min read

How to reduce fraud in loan applications with enhanced risk decisioning

Beat the challenge of fraud in lending with actionable tools, from risk decisioning to authentication solutions with Tink – while getting closer to inclusive loan origination.

Read more

2023-09-01

3 min read

Dennis Dorfmeister & giroAPI – The importance of good frameworks and technical designs

We spoke to Tink Engineering Manager Dennis Dorfmeister, who has been appointed to the advisory board of giroAPI, an open banking initiative led by the Association of German Banks.

Read more

2023-08-30

8 min read

Open finance – Assessing FIDA and its implications

We take a closer look at the European Commission’s FIDA proposal, in particular the pivotal role of Article 4, its implications for data rights, innovation, and the balance between accessibility and affordability for vulnerable consumers.

Read more

2023-08-29

3 min read

Orbyt turbocharges invoicing and direct debits with Tink partnership

Tink and Orbyt partner to offer instant account verification, better direct debits and Pay by Bank-powered invoicing to its customers across Europe.

Read more

2023-08-08

4 min read

An Post releases free money management services with extended Tink partnership

An Post now offers free money management services to all by deepening its partnership with Tink. Just 16 months after joining forces, the An Post Money smart budgeting tool is available to everyone in Ireland, expanding access to the service beyond An Post Money customers.

Read more

2023-08-01

5 min read

Martina Sjöblom - Improving consumer protection with commercial VRPs

Tink Senior Legal Counsel, Martina Sjöblom, has been named to a new sub-working group as part of the Joint Regulatory Oversight Committee’s (JROC) push in the UK to introduce commercial, non-sweeping variable recurring payments (VRPs).

Read more

2023-07-27

6 min read

Banks step up financial management support as Brits seek help to navigate the cost-of-living crisis

New findings reveal an opportunity for banks to enhance consumer support by continuing to develop, and raise awareness of, data-driven financial services.

Read more

2023-07-26

4 min read

SEPAexpress teams up with Tink to scale payments across Europe

SEPAexpress and Tink are teaming up to improve payments for its customers across Europe. Using Tink’s technology, SEPAexpress is simplifying the payment process offering Pay by Bank and instant account and balance verification.

Read more

2023-07-19

7 min read

Financial wellness coaching – how to personalise your digital banking services

Take personalised digital banking into the future with Tink’s Data Enrichment and Money Manager products, based on real-time data and bleeding edge open banking technology.

Read more

2023-07-17

5 min read

Why digital banking services need partners outside banking

Learn why banks need tech partners and ecosystem providers to engage customers, increase loyalty and meet consumer sustainability expectations.

Read more

2023-07-05

2 min read

Make smarter risk decisions with our comprehensive new tool

We have introduced a new feature on the Tink Console called Risk Decisioning, which provides a consolidated risk experience to enhance affordability and risk assessments.

Read more

2023-06-29

5 min read

European Commission introduces PSD3/PSR to advance open banking and strengthen consumer protection

Tink’s Head of Industry & Wallets, Jan van Vonno, discusses the EU's draft legislation for financial services - PSD2's impact, open banking progress, consumer protection, and benefits of the upcoming PSD3/PSR.

Read more

2023-06-28

4 min read

Variable Recurring Payments - New UK working group drive to help accelerate and improve adoption

Tink’s Andrew Boyajian is playing a key role in a new variable recurring payments (VRPs) working group in the UK, advocating for standardisation and faster implementation of this technology in open banking.

Read more

2023-06-21

5 min read

Customer demand for banking tools to track sustainability outstripping supply

New research from Tink shows that an estimated 40% of Brits would like to track their environmental impact through a service provided by their bank – but only 24% of banks currently offer the tools to do this.

Read more

2023-06-15

2 min read

SSP selects Tink as its pan-European partner for open banking payments

Read about how Tink has teamed up with Score & Secure Payment (SSP) to enable open banking payments across the eurozone for its 14,000+ merchants.

Read more

2023-06-13

2 min read

JROC latest - mapping out the UK’s open banking actions

After last week’s announcement of two new working groups formed by the Joint Regulatory Oversight Committee, Tink maps out the latest UK open banking timelines.

Read more

2023-06-07

4 min read

Spotlight - Tink’s fast-growing team in Poland

We spoke to members of Tink’s thriving Polish office, which has expanded from a small engineering hub to a live open banking payments market, with more than 140 staff now based in Warsaw.

Read more

2023-06-01

4 min read

Tink will embed ecolytiq’s solution into its platform to scale sustainability-based services

Tink and climate engagement solution, ecolytiq, are joining forces to embed ecolytiq’s sustainability services into the Tink platform.

Read more

2023-05-25

1 min read

The next era of invoice payments

In this webinar, PostNord Strålfors – the Nordics’ largest distributor of invoices – speaks with Tink to discuss how invoice payments are becoming digitalised.

Read more

2023-05-24

7 min read

How Pay by Bank is approaching its tipping point

Understand how Pay by Bank works as an account-to-account payment method and how to leverage open banking with Tink as it reaches mass adoption.

Read more

2023-05-10

3 min read

Goodlord teams up with Tink to streamline letting applications

Goodlord chooses Tink Income Check to streamline its letting process, using open banking and real-time data to improve verification and minimise fraud.

Read more

2023-05-09

5 min read

Deep dive into spending with Expense Check categorisation

Improve affordability assessment and loan applicant experiences with Tink Expense Check, using real-time data and smart expense categorisation to improve affordability assessment.

Read more

2023-04-26

3 min read

Younited partners with Tink to enable instant lending solutions

Younited and Tink have partnered to streamline credit decisions using open banking. Younited’s data-driven approach to loan origination provides fast, accurate and inclusive lending, simplifying affordability assessments for a smoother experience.

Read more

2023-04-21

5 min read

BNPP Fortis: safeguarding customer trust with budget management tools

An interview with BNP Paribas Fortis' Director of Channels and Customer Experience, Emilie Jacqueroux, on how the bank supports financial wellbeing by providing money management tools to adapt to the cost-of-living crisis.

Read more

2023-04-20

4 min read

Nearly one in four Brits in need of tailored financial support

Tink's latest research shows that almost one in four Brits are in need of tailored financial support. Learn how open banking can help UK banks support financially vulnerable consumers during the cost-of-living crisis.

Read more

2023-04-14

5 min read

How to turn data into personalised customer experiences with categorisation

Data categorisation helps banks clean and categorise transaction data to build better digital banking services, personalise customer experiences and encourage financial wellness. Here’s how to use Tink’s Data Enrichment.

Read more

2023-03-29

4 min read

Optimising open banking experiences for mobile apps

Tink’s new mobile experience optimises the authentication journey and makes integration quicker and easier. Discover how to optimise your app user experiences with our mobile-first approach.

Read more

2023-03-21

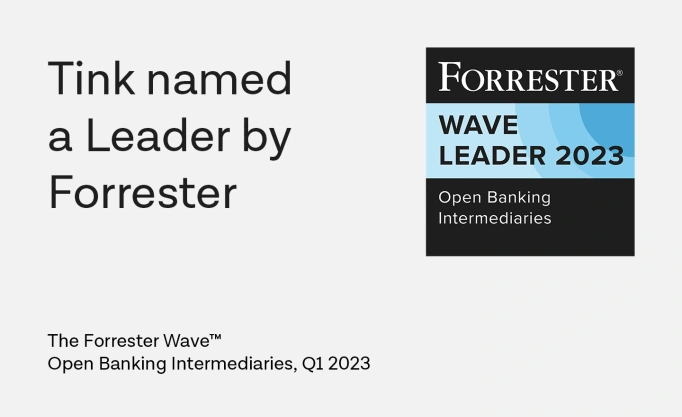

3 min read

Tink named a leader by Forrester

Forrester report ranks Tink a leader in open banking intermediaries: “…a robust, performant solution that can scale.” – read the independent 2023 report here.

Read more

2023-03-21

2 min read

ConTe.it Prestiti partners with Tink for seamless loan origination

Tink and ConTe.it Prestiti team up to power an instant lending application process with open banking, using the Tink Income Check product.

Read more

2023-03-20

6 min read

How banks can offer tailored support to different consumer groups

Different consumers need differing levels of support. Learn how banks can support UK consumers through the cost-of-living crisis by using tailored financial coaching, data-driven tools and money management solutions.

Read more

2023-03-13

4 min read

Multitude Bank partners with Tink for responsible lending processes

Discover how Tink's partnership with Multitude Bank is transforming digital banking across Europe. Streamlining loan origination, improving credit assessments, and promoting responsible lending across 19 countries worldwide.

Read more

2023-03-06

4 min read

Tink tops the Juniper Research Competitor Leaderboard in open banking

Tink tops the 2023 Juniper Research Competitor Leaderboard in open banking – read the independently evaluated report here.

Read more

2023-03-02

11 min read

Small tweaks, big results: accelerating open banking conversion rates

It’s common for friction to appear for users in open banking flows, causing lower completion rates than we would like. See how Tink is working on improving clients’ conversion rates through incremental changes to our products.

Read more

2023-03-01

3 min read

Introducing payment logs inside Tink Console

We’re releasing payment logs – a troubleshooting toolkit within Tink Console that allows you to see the current status of a payment and get more details if and when something goes wrong.

Read more

2023-03-01

5 min read

Under the hood of Early Redirect – turbocharging income verification

How does Income Check make it possible for lenders to verify income in seconds? We went behind the scenes of the Tink tech team to find out how Early Redirect is powering the open banking lending engine. Marcus Elwin, Associate Product Manager, has the details.

Read more

2023-02-23

5 min read

The lenders’ guide to getting started with open banking

Risk decisioning and creditworthiness assessment technology are the tools lenders need to take loan origination into the future. Learn how Tink can help with this guide to optimising affordability assessment.

Read more

2023-02-22

4 min read

Beat the challenge of refunds with Pay by Bank

Online retailers struggling with refunds processes can reduce costs with Pay by Bank. Tink’s open banking tools help businesses optimise both their spend and UX. Read on to learn how real-time payments can help.

Read more

2023-02-14

4 min read

What is pattern recognition and what is it good for?

What is pattern recognition in data enrichment? Learn how Tink Data Enrichment analyses recurring transactions and predicted recurring transactions to help consumers to understand their spending – and banks to improve their services.

Read more

2023-02-09

6 min read

Half of Brits fear budget shortfall – here’s how banks can help

Tink’s latest research shows that a staggering 25 million Brits fear their income soon won’t cover essential costs, meaning banks have the opportunity to support them with tailored banking solutions.

Read more

2023-01-26

4 min read

Meet Data Enrichment: the engine that elevates your banking app

Tink launches Data Enrichment, a new product giving banks the speed and flexibility to innovate digital banking apps, engage customers with PFM and keep them coming back.

Read more

2023-01-18

8 min read

3 ways to accelerate Pay by Bank adoption

Pay by Bank could change the game for your business, helping you add speed and prevent fraud. Learn how open banking powered payments can turbocharge your customer experience.

Read more

2022-12-16

6 min read

The challenges in underwriting and how open banking can help

Digital loan origination processes powered by open banking are often faster, safer and provide a better customer experience than traditional methods – here’s why.

Read more

2022-12-15

4 min read

Why open banking is important for consumers to manage their finances

Give customers actionable ways to stay on top of their finances with Tink’s open banking tools. From personal finance management to inclusive loan origination, make banking and lending processes work for everyone.

Read more

2022-12-14

7 min read

How VRPs can help your customers weather the economic storm

How Variable Recurring Payments can help vulnerable consumers avoid overdraft fees and cancelled payments during the economic crisis.

Read more

2022-12-13

4 min read

How to unlock growth through consumer engagement

Consumer engagement is a crucial component when delivering products and services. Discover the strategies that can help power growth for your business.

Read more

2022-12-08

4 min read

How Pay by Bank can help struggling merchants as recession looms

Tink’s latest research shows that half of UK online retailers are worried about surviving the next 12 months, as recession looms. Here’s how Pay by Bank can help.

Read more

2022-12-06

3 min read

Closing the data gap for affordability assessment

Quality affordability assessment and creditworthiness are key to the future of lending. Learn how Tink’s open banking platform closes the data gap for lenders and encourages responsible lending.

Read more

2022-12-02

4 min read

The European Payments Council’s first SEPA Payment Account Access (SPAA) rulebook – the Tink take

The European Payments Council’s first SEPA Payment Account Access (SPAA) rulebook was published this week. Tink provides a summary and view on the latest developments.

Read more

2022-11-30

9 min read

How VRP is sweeping money management into a new era

Sweeping VRPs, the me-to-me payment method that is simplifying money management for businesses and consumers.

Read more

2022-11-28

6 min read

How Money Manager helps you boost customer loyalty

Personalisation is essential to engaging customers and building loyalty for banking apps. Tink’s Money Manager has the features to help.

Read more

2022-11-24

5 min read

Balance Check

Reducing fraud and failed payments just got easier. Learn how balance check is increasing operational efficiency and reducing chargebacks.

Read more

2022-11-23

5 min read

Instant refunds and withdrawals are here

Tink’s payments upgrade adds instant refunds and withdrawals, letting businesses across Europe issue payouts that settle in less than one second.

Read more

2022-11-21

12 min read

How to achieve the best possible Pay by Bank conversion rate

When making a purchase online, consumers look for simple, safe and convenient payment experiences. In this guide, our Payments team shares its best practices for optimising Pay by Bank user journeys and ensuring the highest possible conversion rate.

Read more

2022-11-17

2 min read

Open banking solutions to meet digital-savvy customer expectations

The modern customer expects more from their service provider than ever before. Discover how open banking can help you satisfy their needs in our ultimate solutions guide.

Read more

2022-11-04

2 min read

How open banking is reducing risk and powering more inclusive lending

Lenders can approve more loans while taking less risk with the help of open banking. Learn more about risk decisioning in our ultimate solutions guide.

Read more

2022-11-02

5 min read

Introducing Tink’s Variable Recurring Payments beta programme

Tink and NatWest have partnered up to launch a beta VRP programme in the UK to gather real use cases for merchants based on their needs.

Read more

2022-11-01

8 min read

What’s a good Pay by Bank conversion rate?

Comparing Pay by Bank conversion rates across different payment methods can be tricky since most don’t use an end-to-end metric. See Tink’s own benchmarks and how we track performance in this conversion rate deep-dive.

Read more

2022-10-31

7 min read

Consumer lending in times of uncertainty

Discover what lies ahead for lending in these uncertain times – and how you can adapt to today’s needs.

Read more

2022-10-28

3 min read

The European Commission’s Instant Payments proposal – the Tink take

The European Commission published its proposal on Instant Payments clearing the way for widespread adoption of open banking payments.

Read more

2022-10-27

8 min read

Investment platforms: what to look for in an open banking partner

Looking for the best open banking provider? Here is everything you need to consider before making a decision.

Read more

2022-10-26

3 min read

Sambla partners with Tink for a more inclusive lending process

Tink and Sambla partner up to offer better, more inclusive affordability analysis for all types of loan applicants.

Read more

2022-10-24

1 min read

Unlocking a new era of credit

In this webinar, Christophe Joyau, Tink SVP Banking and Lending, and David Öhlund, CEO Scandinavia GF Money, discuss how open banking is transforming the lending landscape.

Read more

2022-10-21

5 min read

How to create a digital-first invoice payment experience with ease

Whilst some invoice distributors are still using time-consuming, traditional analogue flows, open banking is transforming the invoice payment experience. Learn how to easily digitalise existing analogue flows using Tink payment technology.

Read more

2022-10-14

3 min read

Tink and Zervant partner for faster invoice payments

Tink and Zervant have partnered up to enable open banking payments for invoicing for over 100,000 SMEs.

Read more

2022-10-13

4 min read

Instantly verify income with Income Check – now with new features

To help businesses make informed and accurate decisions when assessing applications, we’ve made it even easier for them to instantly verify an applicant’s income with the use of granular, up-to-date data. All with just a few simple clicks.

Read more

2022-10-12

2 min read

The solutions that are transforming the payments landscape

The modern customer wants a frictionless payment experience. Discover how open banking payments can help you in our ultimate solutions guide.

Read more

2022-10-11

5 min read

How evolving digital expectations are creating new opportunities for banks

With Tink’s Data Enrichment, banks gain access to enriched and personalised consumer spending insights – enabling them to better support their customers’ digital needs.

Read more

2022-10-06

5 min read

How telco and utility companies are using open banking to navigate economic uncertainty

Open banking is helping telco and utility companies navigate these uncertain times by focusing on quicker onboarding, faster payments and better affordability checks. Learn how open banking can help you.

Read more

2022-10-05

3 min read

Tink and Adyen partner for open banking payments

The global fintech platform Adyen is partnering with Tink to power its new pay-by-bank solution and offer instant bank payments to its customers. The partnership will help accelerate the global adoption of open banking powered payments.

Read more

2022-09-29

5 min read

The key to unlocking fairer and more responsible lending

In our latest report, we explore how open banking can pave the way for faster, safer, and more responsible lending practices – and what lenders can do to prepare for this new era of credit.

Read more

2022-09-22

10 min read

The truth about Variable Recurring Payments: current status, use cases, and future prospects

Many claim Variable Recurring Payments (VRPs) are changing the payments landscape. But what’s the actual status? And are there already viable use cases? We try to cut through the noise and explore the challenges and opportunities of VRPs.

Read more

2022-09-15

4 min read

Under the hood: building a new Tink product

We look under the hood to find out how the Tink tech team tackles the challenges of building our latest lending product, Expense Check – a feature that allows you to assess affordability with facts rather than assumptions.

Read more

2022-09-07

2 min read

Affordability solutions that are leading the way in lending

Affordability and lending. Discover how open banking can help you get a more accurate picture of a potential borrower’s creditworthiness in our ultimate solutions guide.

Read more

2022-09-06

4 min read

SlimPay partners with Tink

SlimPay is partnering with Tink to offer seamless subscription payment experiences across Europe, powered by open banking. SlimPay merchants will be able to offer a secure, seamless way to set up a direct debit that lets users authenticate and make the initial payment through open banking.

Read more

2022-08-31

5 min read

Improved affordability assessments with Expense Check

Tink’s new product Expense Check enables lenders to accurately assess applicant’s affordability with open banking. With real-time, granulated expense data, lenders can check the applicant’s creditworthiness in a matter of minutes.

Read more

2022-08-25

3 min read

Billogram and Tink partner to streamline invoice payments

We’re proud to announce a partnership with Billogram to further improve their customer experience by removing friction from their invoicing platform.

Read more

2022-08-24

6 min read

The top 3 trends driving open banking payments adoption today

Faster, broader coverage, and higher security: the top 3 trends driving open banking payments adoption today, according to industry leaders.

Read more

2022-08-18

10 min read

The key to picking an open banking payments partner: bank coverage

The key to picking the right partner for open banking payments is connectivity. Bank on better coverage to help you scale in the best possible way.

Read more

2022-08-16

2 min read

The solutions that will lead to a new world of finance

Discover the open banking solutions that are leading to a new world of finance.

Read more

2022-08-11

2 min read

Get ready for better digital affordability assessments

How open banking can help simplify and improve digital affordability assessments.

Read more

2022-08-04

5 min read

Charlotte Hogg @ Money2020 – five quotes on the future of open banking

What lies ahead for the future of open banking? Five Money 20/20 quotes from Visa Europe CEO, Charlotte Hogg

Read more

2022-07-27

6 min read

3 easy ways to turn financial data into value

The democratisation of financial data is opening up new opportunities. Find out how to harness its power with open banking in our latest article.

Read more

2022-07-21

5 min read

28% of self-employed struggle to access financial services

Self-employed workers are being left out of financial services. Here’s how open banking can help.

Read more

2022-07-18

5 min read

Solidi and Tink partner to launch instant account top-ups for crypto investors

Tink is partnering with UK cryptocurrency exchange Solidi to bring instant payments settlements to crypto investors. Open banking-enabled account settlements are faster, safer, and more convenient than bank transfers.

Read more

2022-07-14

4 min read

How open data can help tackle the cost-of-living crisis

The cost of living is reaching an all-time high for many. Read on to find out how data can help consumers navigate these turbulent times – thanks to the near limitless possibilities of the open data economy.

Read more

2022-07-13

6 min read

Settlement accounts

Tink launches settlement accounts for simpler instant bank payments to speed up settlement times and reduce the risk of fraud. First launch in collaboration with UK crypto exchange, Solidi. Find out how it can help reduce friction in your business.

Read more

2022-07-05

11 min read

Lessons from taking open banking payments mainstream: an interview with Billy Telidis

We caught up with Billy Telidis, Product Manager of Payments at Tink, to talk about how open banking payments have gone from relative obscurity to a preferred payment method.

Read more

2022-06-30

4 min read

How Again is using transaction data to drive change

Using open banking to drive sustainable change: Swedish climate fintech Again is partnering with Tink to end greenwashing. Their app leverages transaction data to accelerate the climate transition by offering valuable user data to sustainable brands.

Read more

2022-06-28

11 min read

Debunking the 5 biggest myths about Pay by Bank

Curious about what's true and what's false about open banking payments like Pay by Bank? Let's cut through the noise and bust some of the most persistent myths.

Read more

2022-06-22

7 min read

What’s the difference between A2A payments and PIS? In short: open banking

A2A payments are said to be faster, safer, cheaper than other payment methods. The term PIS, or payment initiation services, often gets thrown around in the same context. So how do they differ? In short: through open banking.

Read more

2022-06-16

7 min read

Why invoices are the perfect use case for open banking payments

What makes open banking such a good match for invoice settlement, and how can this product-market fit help lead to mass adoption? We take a look at a use case to find out.

Read more

2022-06-07

2 min read

Revolut and Tink partner for European payments

The global financial super app Revolut has entered into a strategic partnership with Tink to offer its European customers seamless payment solutions powered by open banking.

Read more

2022-06-02

6 min read

The regulatory requirements in store for lenders – and how open banking can help

In the wake of the pandemic and the digital transformation of finance, consumers are borrowing money they can’t afford to pay back. But open banking holds the key to safely assess applicants’ creditworthiness.

Read more

2022-05-31

4 min read

A new generation of payments is taking shape – powered by open banking

Tink survey reveals financial executives in Europe consider security, speed, and low cost as top benefits of payment initiation services – but that barriers to full-scale adoption remain.

Read more

2022-05-24

5 min read

How banks can add value for their customers with recurring transactions

With so many subscription services popping up, consumers are losing control of their recurring costs. Find out how banks can leverage open banking – and Tink’s data enrichment capabilities – to help them better manage their finances.

Read more

2022-05-18

5 min read

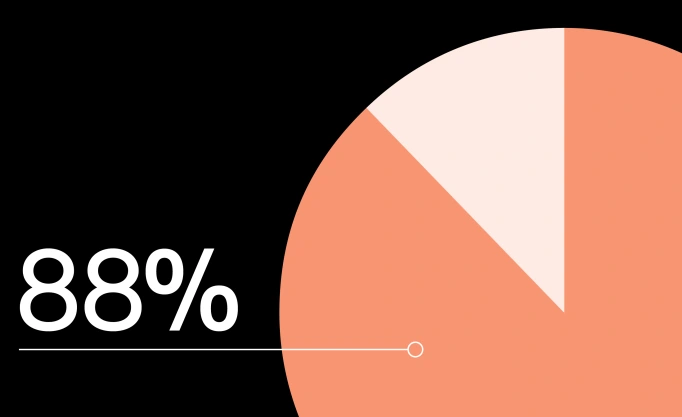

UK consumers expect fast and frictionless payment journeys

Tink’s latest UK survey shows that nearly 9 in 10 consumers (88%) are prepared to abandon a transaction if faced with friction when making a payment online, highlighting the need to ramp up payments innovation and focus on user experience

Read more

2022-05-17

6 min read

Build vs buy – a lender’s guide to the pros of partnership

In today’s digital world, it’s all about data – and the seamless user experiences it can power. Learn about the importance of real-time data, optimal UX, and more in this guide to building vs buying.

Read more

2022-05-11

4 min read

Get to know the tech behind better risk assessments

Open banking can help make better informed risk decisions – but access to data is just a part of the puzzle. Find out why quality account aggregation and data enrichment are the foundations of a standout risk assessment process.

Read more

2022-05-10

4 min read

The evolution of the revolution – from open banking to open data economies

It’s time to move on from just talking about open banking. Tink's latest report shows that data is on the agenda – open banking is evolving into open finance, which in turn is readying the market for the creation of open data economies.

Read more

2022-05-03

4 min read

Invoice settlement: what it is, and how open banking makes it simpler

Paying bills and invoices has typically been a cumbersome process – but thankfully, open banking can make it a lot quicker and easier by allowing customers to pay directly from their bank account. Here’s how that works.

Read more

2022-04-28

4 min read

How open banking risk assessments can impact consumers’ lives

It’s no secret that traditional credit checks don’t always work for everyone – but open banking can boost financial inclusion, giving more people access to credit, and fairer results thanks to better risk assessments. Here’s how.

Read more

2022-04-20

4 min read

A simple way to improve risk decisioning

Having a more holistic picture of someone’s financial situation can make all the difference when it comes to making well-grounded risk decisions. Luckily, open banking makes it a lot easier to build strong risk profiles. Here’s how.

Read more

2022-04-01

3 min read

How Lumify cut their loan application time by half with open banking

Lumify partners with Tink to improve customer experience. With the help of open banking, Lumify has cut loan application processing time by more than half – with a 40% increase in success rate. Here’s how.

Read more

2022-03-31

7 min read

Young people in the UK call for banks to help them go green

Tink research finds that 18-34 year olds in the UK want more information on their carbon footprint, and place high expectations on banks to help them track and improve it. With open banking, financial institutions can meet this demand.

Read more

2022-03-24

17 min read

Lender's guide to improving risk assessments with open banking

We dive into the world of risk assessments, exploring challenges lenders face with current decisioning methods, and how the process can become more convenient, reliable and complete thanks to open banking and the smart use of data.

Read more

2022-03-23

8 min read

Are open banking payments taking off? How businesses and consumers are already reaping the rewards

Tom Pope, head of payments and platforms at Tink, lifts the lid on where open banking payments scale is coming from – and whether the world is ready.

Read more

2022-03-17

6 min read

Unsure how open banking payments can help your business? We can show you where they’re booming

Tom Pope, head of payments and platforms at Tink, explains where open banking payments are gaining the most traction – and why the big opportunities are emerging now.

Read more

2022-03-16

4 min read

Beyond PIS – different ways payments can benefit from open banking

Explore the different ways to leverage open banking technology in payments – beyond A2A and PIS. Enable seamless onboarding with instant account verification, and reduce fraud and nonpayments with real-time balance check.

Read more

2022-03-15

3 min read

PostNord Strålfors and Tink partnering for payments

Find out how PostNord Strålfors – the largest distributor of invoices in the Nordics – is transforming how invoices are paid. (Spoiler alert: it has to do with their new partnership with Tink.)

Read more

2022-03-15

6 min read

Behind the scenes of an award-winning open banking partnership

Tink partner NatWest was awarded the Celent Model Bank 2022 Award for its Digital Spending feature. We talked to partnership insiders to get their views on the collaboration, and what it takes to build a successful partnership.

Read more

2022-03-03

3 min read

How mozzeno’s sharing economy marketplace is benefitting from open banking

Belgian fintech mozzeno partners with Tink to simplify their onboarding process with the help of open banking. The result is a collaborative marketplace that saves users time and unnecessary paperwork.

Read more

2022-03-01

3 min read

An Post and Tink team up to simplify money management for Irish customers

An Post, Irish postal service provider, is partnering with Tink to give its customers the power to better manage their money. Using Tink’s open banking technology, An Post’s Money Manager app helps users improve their finances.

Read more

2022-02-25

4 min read

Introducing customisable logos and desktop layout inside Tink Link

Tink Link's new customisable headers blend into your authentication flow and make the customer journey more cohesive. The new desktop layout provides a better user experience with increased readability and accessibility.

Read more

2022-02-23

3 min read

How Findity simplifies expense management with open banking

Expense management provider Findity is partnering with Tink to improve the expense management process for businesses and employees alike. Here’s how they’re tapping into open banking to simplify everyday life and cut down on work admin.

Read more

2022-02-16

6 min read

3 ways open banking can promote sustainability

There are many ways in which open banking can help promote sustainability, for businesses as well as consumers. Find out how to create better digital experiences, increase efficiency, and save the planet – all at the same time.

Read more

2022-02-09

3 min read

Youtility and Tink partnering to simplify subscriptions and sustainability

Youtility and Tink are teaming up to help retail banks in the UK offer subscription and money management tools – with savings and sustainability in mind. Here’s more about the partnership, and how it’s addressing important consumer needs.

Read more

2022-02-03

4 min read

Introducing a new no-code integration for Tink Link

Integrating Tink's products just got easier with an option that lets you skip having to write code. Here’s what you need to know about the new feature – Standalone Tink Link – and some of the improvements that come with it.

Read more

2022-02-02

4 min read

Open banking vs open finance – what’s the difference?

We explore the difference between open banking and open finance, as well as the possibilities that come with an open financial services landscape. Such as better-tailored financial services and improved financial health.

Read more

2022-01-27

3 min read

Mobify partners with Tink to create more value for its users

Payment and invoicing platform Mobify wanted to expand their offering and give Finnish consumers an even more comprehensive – and personalised – finance management experience. Here’s how they’re partnering with Tink to do it.

Read more

2022-01-25

4 min read

HomeQ: making renting seamless with instant income verification

Find out how Swedish rental marketplace HomeQ is simplifying life for tenants and landlords alike – and how they’re leveraging open banking to provide a seamless application process thanks to instant income verification.

Read more

2022-01-20

6 min read

Making way for open finance: insights from the EU Commission

We had a chat with Mattias Levin, Deputy Head of Unit at the EU Commission, about the pandemic boom of digital finance, the future of open banking, and using policy to aid post-pandemic economic recovery.

Read more

2022-01-19

3 min read

NatWest, Cogo and Tink: a three-way partnership to boost sustainability

NatWest enlisted the help of both Tink and Cogo to offer a carbon tracking feature for their climate-conscious customers. Here’s how it works – and why Tink and Cogo joined forces to bring other similar solutions to market.

Read more

2022-01-04

4 min read

Where is open banking heading? – our predictions for 2022

While we can never really know for sure what the new year will bring – it’s still quite fun to guess. (Then look back to see what you got right and where you were way off.) Here’s what Tink CEO Daniel Kjellén predicts for 2022.

Read more

2021-12-16

4 min read

3 tips to keeping a competitive edge as new entrants move into financial services

Open banking is ramping up competition in the financial services space, as new market entrants start capitalising on the opportunities. How can financial incumbents make sure they remain on top of the game? Here’s what we suggest.

Read more

2021-12-08

7 min read

Performance analytics

The Tink Console has a hot new feature: get deeper insights into how your open banking flows are performing in almost real time, including overall completion rates, conversion at different steps and drop offs or errors per bank.

Read more

2021-12-02

3 min read

How ecolytiq is supercharging their sustainable banking solution with Tink

Once again, open banking data is being used to save the world and help people reduce their environmental impact. Find out how ecolytiq is supercharging their sustainability solution for banks and fintechs by partnering with Tink.

Read more

2021-11-25

1 min read

Guide to account verification solutions

Learn all about the most common account verification methods used today, why they don’t always meet today’s digital customers’ expectations – and how you can use open banking to provide a faster, safer, and simpler solution.

Read more

2021-11-23

2 min read

Open banking investments and use cases

How has the pandemic impacted open banking budgets? How much did financial executives invest in their open banking objectives? And which opportunities do they have in sight? We surveyed bankers across Europe to find out.

Read more

2021-11-22

6 min read

Improve risk assessment and application processes with data-driven Risk Insights

Creating detailed risk profiles can be hard. But we have a new product to solve that. Find out how Tink’s Risk Insights is giving lenders more information to go on – while also improving the application process for consumers.

Read more

2021-11-17

3 min read

Open banking investments: are billions in revenue at stake?

Open banking brings an opportunity to improve the value propositions in payments, retail banking, wealth management, insurance, investments and other segments of finance. But how much could this opportunity be worth, exactly?

Read more

2021-11-11

5 min read

Why UX is crucial – and how you can improve performance with Tink

Is your Tink integration providing the best possible user experience? After working with customers to improve performance, we’ve identified small UX changes that can make a big difference. And we created a guide to help out.

Read more

2021-11-02

5 min read

The benefits of tapping into business account data with Business Transactions

New product alert: with Tink’s Business Transactions, you can easily and safely access real-time transaction data from business accounts. Here’s how it works, and some of the most common challenges it can help solve.

Read more

2021-10-28

10 min read

SEPA Request-to-Pay: what you need to know about the new scheme

What is the SEPA Request-to-Pay scheme? What does it mean for banks, merchants and consumers – and for the future of payments in Europe? Is there anything that might be holding it back? We provide answers – and our own take on it.

Read more

2021-10-26

5 min read

3 ways accountancy services can take advantage of open banking

Is open banking a threat to the accounting industry? We don’t see it that way. In fact, we think accounting software providers have a lot to gain by leveraging new open banking capabilities. We take a look at some of the key benefits.

Read more

2021-10-19

3 min read

How Gimi is promoting financial education for children with open banking

Find out how Swedish startup Gimi is teaching kids about basic personal finance concepts while empowering them to better handle their finances – and how open banking comes into the mix as a fundamental piece of the puzzle.

Read more

2021-10-14

5 min read

Emerging open banking strategies

To expose, or consume open banking APIs? That is the question. Discover the four paths financial institutions can take when it comes to their open banking strategy, and our view on what is currently the best route to explore.

Read more

2021-10-12

8 min read

Open banking use cases beyond financial services

Open banking isn’t just changing the game for financial services. Find out how different industries, from retail to telcos, can take advantage of the free flow of financial information to improve customer experiences – and business results.

Read more

2021-10-08

3 min read

eCollect partners with Tink to streamline receivables management across Europe

Find out how eCollect is simplifying and digitising invoice payments – and how their new partnership with Tink will help ensure hassle-free cash management for their customers and a seamless experience for end users.

Read more

2021-09-30

8 min read

Inside Tink: getting top model performance for Income Check

How do you improve a classification model to sort out what’s an income and what isn’t? Tinker Ida Janér reveals how data scientists in the Risk team embraced confusion and took in regional differences to optimise performance.

Read more

2021-09-23

3 min read

Serrala partners with Tink to offer improved bill payments across Europe

We’re partnering with global financial automation and payments company Serrala to simplify the billing process and reduce transaction fees for billers while improving the payment experience for millions of consumers across Europe.

Read more

2021-09-21

3 min read

Bankers embrace the open banking revolution – but expect a long journey ahead

Financial executives in Europe see open banking as a revolution, and are embracing it more than ever. But many expect it will take several years to get there. While transformation takes time – there could be a way to accelerate it.

Read more

2021-09-16

3 min read

Lemonway and Tink partner to offer smarter digital payments for marketplaces

Lemonway, a French payments service provider, launched their Pay By Bank with Tink, a new service that allows their merchants to offer users an easy, secure, and convenient digital payment method.

Read more

2021-09-14

5 min read

Why is the UK so good at open banking?

The UK’s open banking journey has been a bit different compared to other countries in Europe, and this has given them an edge – leading to a more mature environment. Here’s our take on what has contributed to their success.

Read more

2021-09-09

4 min read

How Gokind is combating greenwashing with open banking

Discover how Swedish startup Gokind is cleverly combining users’ financial data with sustainability information from brands to help consumers understand the real impact of their purchases and make more ethical choices.

Read more

2021-09-08

3 min read

Placons – a personal financial butler

Personal finance management (PFM) app placons wanted to rethink what a bank actually could do for its users. Here’s how they’re using Tink’s Money Manager to help their users lead a more financially sustainable lifestyle.

Read more

2021-09-01

6 min read

New priorities for bankers – and how open banking can help

Banking priorities have changed as a result of the pandemic. Discover the three focus areas that are top of mind for financial executives – and how open banking can help institutions tackle all three by leveraging financial data.

Read more

2021-08-26

8 min read

Inside Tink: changing our approach to outlier detection

Learn how data scientists in Tink’s Enrichment Categorisation team improved categorisation results by changing their approach to detecting outliers. Tinker Eliisabet Hein gets into the technical details and takes us through the change.

Read more

2021-08-25

4 min read

How epap is using transactional data for sustainable finances

epap is on a mission to reinvent the paper receipt with a digital and more sustainable way to keep track of receipts – all in one app. By partnering with Tink, epap can offer their users an easier and more efficient digital receipt experience.

Read more

2021-08-19

5 min read

Why connecting to open banking APIs is not as simple as it seems

Connecting to an open banking API seems pretty straightforward. But making the connection is just the first step in a complex process. Here are some aspects businesses often overlook when deciding to build the connections in-house.

Read more

2021-07-13

5 min read

The UK leads the way in seeing the digital shift caused by Covid as permanent

Tink’s new survey report finds that a majority of financial executives in the UK foresee a permanent impact from the pandemic – unlike their European peers. We take a closer look at the UK stats, and how they compare to the EU-wide results.

Read more

2021-07-07

4 min read

How open banking simplifies income verification

Income verification used to mean having to dig up bank statements, share income tax statements or payslips – and then wait days or even weeks to have it all verified. Now, thanks to open banking it can take seconds. Here’s how.

Read more

2021-06-24

3 min read

Tink is joining Visa

We are thrilled to announce Visa is acquiring Tink. This is the beginning of a new chapter in open banking, and we couldn’t be more excited about what this means for our employees, our customers and the future of financial services.

Read more

2021-06-17

3 min read

Tink and Novalnet enter European partnership for real-time merchant payments

We’re partnering with German payments provider Novalnet to take real-time, open banking powered payments across Europe, starting with Germany and the UK, enabling merchants to receive transactions almost instantly.

Read more

2021-06-17

1 min read

Open banking in the post-pandemic world

Tink’s Research Director Jan van Vonno dives into the findings from our 2021 report, sharing economic statistics and survey results to shed light on emerging risks, changing priorities, and the role of open banking in the years ahead.

Read more

2021-06-16

5 min read

What is a payment account according to PSD2?

What is considered a payment account under PSD2 and what isn’t? Seems like a simple question, right? But, as with most topics in the finance industry, the answer is almost always ‘well, it depends…

Read more

2021-06-15

4 min read

Banking executives see an irreversible digital shift caused by Covid

In our new report ‘open banking in a post-pandemic world’ 41% of Europe’s financial executives believe the digital shift caused by Covid is permanent – with over two thirds saying the pandemic has increased their focus on open banking.

Read more

2021-06-01

6 min read

3 ways lenders can take advantage of open banking

Find out how the lending industry can benefit from open banking, and how they can leverage new tech capabilities to improve the user experience, reduce costs, increase operational efficiency and optimise results.

Read more

2021-05-26

3 min read

Tink and Wealthify partner for open banking payments

Tink and Wealthify are partnering for open banking payments to transform how Wealthify investors transfer money into their accounts, providing a seamless, faster and more cost-effective payment experience.

Read more

2021-05-19

6 min read

How Sigmastocks optimised their onboarding in less than 4 weeks

Find out how Sigmastocks is simplifying investments, and how open banking is helping them streamline their account verification to speed up customer onboarding.

Read more

2021-05-18

3 min read

Tink acquires leading German open banking tech provider FinTecSystems

Tink has acquired FinTecSystems – a leading German open banking tech provider, powering over 150 banks and fintechs. The acquisition will offer customers in the DACH region the most complete solution when partnering for open banking.

Read more

2021-05-12

7 min read

Open banking glossary: the ABCs of PSD2

Many of the acronyms used in open banking were introduced in connection with PSD2, and they can be a little confusing. This means it’s important to explain them, otherwise, people might have a hard time following you.

Read more

2021-05-11

2 min read

Tink and American Express launch open banking partnership

Tink and American Express are partnering to improve the onboarding process for prospective card members in Europe, by using open banking technology to instantly verify identity, income and account information.

Read more

2021-05-07

2 min read

Lydia expands across Europe with Tink – launching in Portugal

Lydia is expanding its open banking partnership with Tink to Portugal, enabling its users to gather their accounts in one place, make contactless payments and online purchases, and transfer money to friends.

Read more

2021-05-06

5 min read

Instantly verify customers’ income with Income Check

Most income verification methods used today cause friction and delay in the application process, and they’re not even that reliable. Here’s how open banking lets this process finally catch up with the digital age.

Read more

2021-05-05

4 min read

Tink and Tribe partner for open banking payments

We’re teaming up with Tribe for open banking technology, enabling Tribe to combine issuer and acquirer services with Tink’s open banking payments – so Tribe’s customers can access both traditional and more innovative payment solutions.

Read more

2021-04-29

10 min read

All about Variable Recurring Payments, and how they can accelerate innovation

Variable Recurring Payments is a hot topic in open banking, and many believe it could change the face of consumer payments as we know them. Here’s an overview of how it works – and why it’s such a powerful contender in the payments space.

Read more

2021-04-28

4 min read

Why Tink picks Poland for its biggest ever engineering expansion

Tink’s Warsaw engineering hub is booming, and we’re hiring 60 new engineers to more than double the hub in 2021 – to help lay the foundations that the future of Europe’s financial services will be built upon.

Read more

2021-04-27

7 min read

Inspiration from some of the (10,000+) developers on the Tink platform