Financial institutions prioritise payments and customer experience as open banking spending grows

Tuesday 30 November 2021: New research published by open banking platform Tink reveals an increase in spending among Europe’s financial executives, with 47% saying their open banking budgets have risen in 2021. This follows a challenging year in 2020, where financial institutions battled budget restrictions against the race to serve more customers digitally.

Tink’s research – based on 308 senior decision makers at financial institutions in 12 European countries – found the Covid-19 pandemic impacted budgets for 93% of financial institutions, with almost a quarter (23%) revealing the impact was significant. At the beginning of 2020 executives expected to spend, on average, €50-100 million on achieving their open banking objectives. With the huge challenges of the pandemic, the average spend landed at €32 million in 2020.

Retail banks and wealth management firms bucked this trend – spending, on average, €84 million and €79 million respectively on their open banking objectives in 2020. This discrepancy in budget allocation was likely driven by the need to put significant investment towards the creation of compliant PSD2 APIs, as well as the task of overhauling legacy infrastructure to meet current and future open banking needs.

2021 investments fuelled by the shift to digital

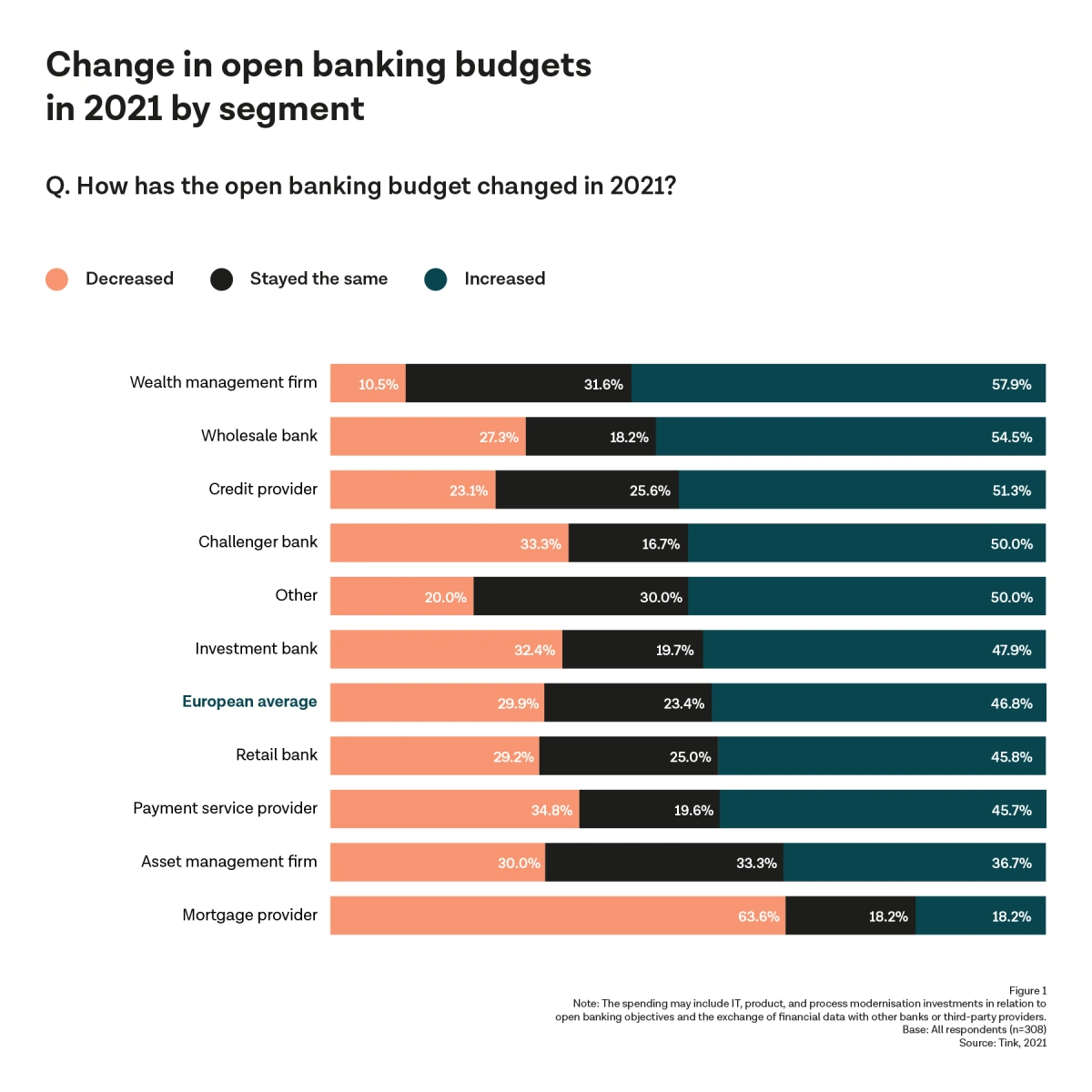

A breakdown of the data reveals how open banking investments have increased during 2021, with wealth management firms experiencing the strongest increase in budgets (58%). This is followed by wholesale banks (55%), credit providers (51%) and challenger banks (50%).

Figure 1: Open banking budgets — percentages illustrate how open banking budgets have changed in 2021 by segment.

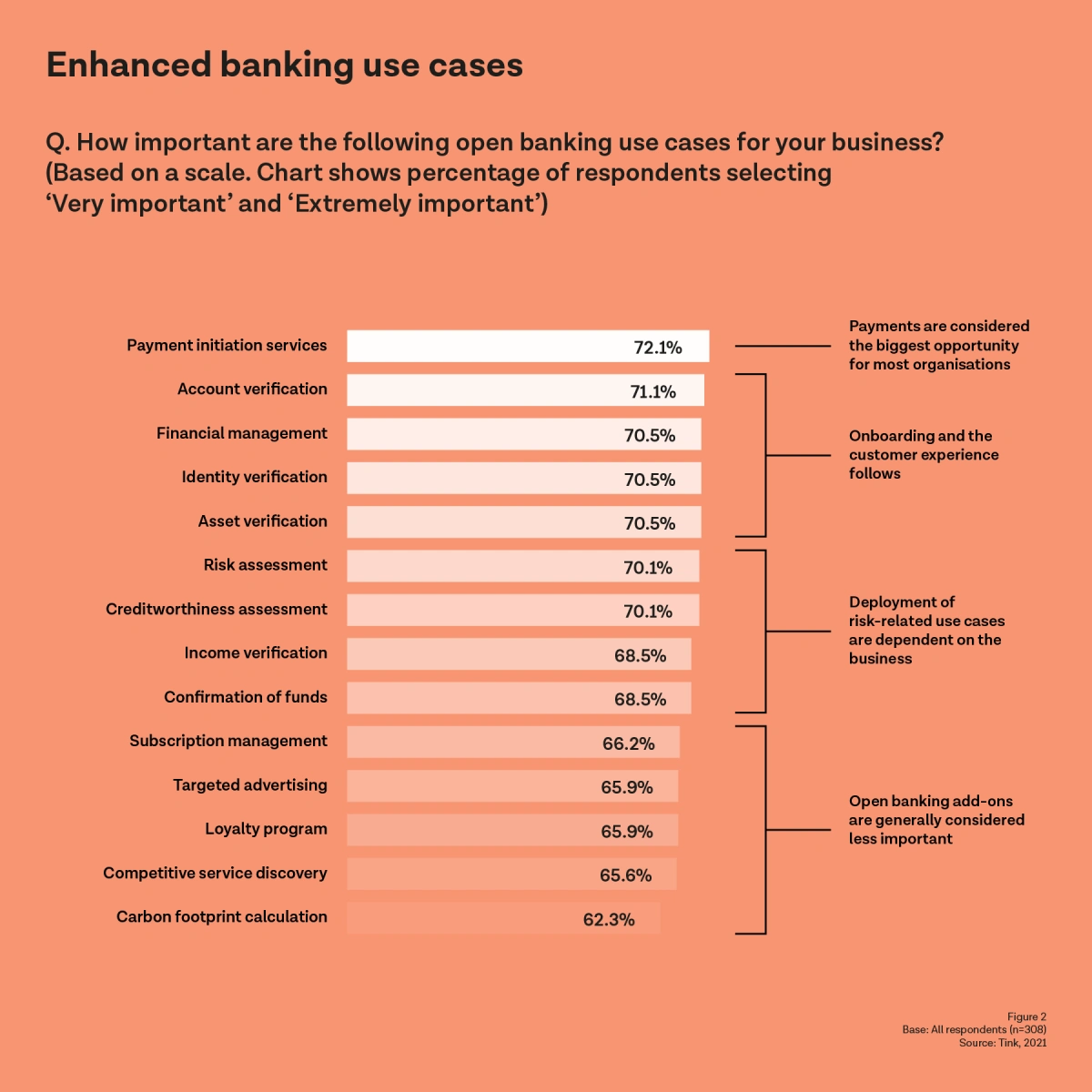

When we look deeper into the areas these investments are being prioritised towards, Tink’s findings reveal that payment related services top the spending priorities in 2021. Specifically, 72% of financial institutions see payment initiation services as the most important use case to their business. This suggests increasing awareness of the need to develop payment solutions that provide more streamlined services for customers.

Improving the customer experience and onboarding process was the second most important area of enhanced banking use cases this year – with account verification, identity verification and asset verification equally weighted amongst 71% of executives. These use cases not only make it easier for banks to make more informed credit decisions for their customers, due to the real-time, holistic view of their data, they also make it simpler for users to switch or sign up with new financial services providers.

The deployment of risk-related use cases is also considered extremely important, with risk and creditworthiness assessments a priority for over two thirds (71%) of financial executives.

Figure 2: Open banking use cases — percentages illustrate respondents selecting use cases as 'Very important' and 'Extremely important for their business’

Although carbon footprint calculation appears at the bottom of the list, it’s still a highly relevant use case for most respondents (62%) – particularly when you look at the retail banking segment, where it ranked as the fourth top priority overall.

Daniel Kjellén, co-founder and CEO, Tink, said: “As open banking moves towards mainstream adoption we’re not surprised to see investments in data-driven initiatives increasing. Financial executives have set their sights on a broad range of open banking use cases, from payments to credit assessments to carbon tracking, unleashing a new wave of value creation that both consumers and businesses will benefit from.

“As we look to 2022, the findings of this report suggest that financial institutions should move fast, as open banking is tearing down barriers and allowing new players to enter the market. To keep a competitive edge, it’s important to focus on enhancing the core business, and consider working with partners to create open banking solutions that can drive value across all areas of financial services. Creating an ecosystem of players that work together will be crucial as we move towards a new age of digitalisation and enhanced customer experience.”

To download the report, please go to: tink.com/survey-reports/investments-use-cases

— ENDS —

Contact details:

Linda Winder, PR & Communications Director, +46 8 509 08 999, press@tink.com

About the research

For the third year in a row, Tink worked with YouGov to conduct a wide-ranging survey on the attitudes and opinions towards open banking in Europe. All interviews were conducted by YouGov between February 25 and March 27th 2021, and included 308 prominent financial services executives spread across 12 countries.

The participants answered questions through telephone interviews and an online questionnaire.

To be selected for the survey, participants needed to be i) senior decision makers or influencers, ii) employed by a regulated financial institution, iii) have confident knowledge of PSD2, and iv) have insight into the open banking investment plans.

About Tink

Tink is Europe’s leading open banking platform that enables banks, fintechs and startups to develop data-driven financial services. Through one API, Tink allows customers to access aggregated financial data, initiate payments, enrich transactions, verify account ownership and build personal finance management tools. Tink connects to more than 3,400 banks that reach over 250 million bank customers across Europe. Founded in 2012 in Stockholm, Tink’s 500 employees serve more than 300 banks and fintechs in 18 European markets, out of offices in 13 countries. We power the new world of finance. For more information, visit tink.com.